A Safe Harbor for the Fed

Shielding the Fed from Politics and Uncertainty

This week on Macro Musings, I spoke with Kathryn Judge, a professor at Columbia Law School, about her new paper coauthored with Rich Clarida on the Federal Reserve’s emergency lending authority. The paper takes stock of the Fed’s use of its Section 13(3) facilities during both the Global Financial Crisis and the COVID-19 pandemic, highlighting how these tools evolved in design and purpose across the two episodes.

Although the core legal authority under Section 13(3) remained intact, it was meaningfully revised by the Dodd-Frank Act following 2008. These changes tightened the conditions under which the Fed could lend, including requirements for broader eligibility and Treasury sign-off, but still left room—particularly with Treasury backing—for a forceful response in 2020. Kate and Rich argue that this Treasury-Fed partnership, in which the Treasury absorbed first losses and signaled political support, enabled the Fed to act more boldly while preserving its monetary independence. Kate emphasized on the podcast that such a partnership should be seen not as a threat to the Fed’s credibility, but as a strength—a means of integrating the central bank into a coordinated, whole-of-government crisis response while still protecting its core responsibilities, especially in monetary policy.

Looking ahead, Kate expressed support for expanding the Treasury’s role even further, not necessarily through 13(3) itself, but through the creation of alternative emergency mechanisms—such as short-term government guarantee programs—that would ease pressure on the Fed and allow it to stay focused on its core monetary and lender-of-last-resort functions. For her, the best way to preserve the Fed’s independence may be to narrow the scope of what we expect it to do during times of crisis. She makes this point in the video clip below:

Kate and I also discussed institutional developments that could reshape the Fed’s role and autonomy. These include recent executive actions to increase White House oversight of independent agencies, proposals to shift bank regulatory powers away from the Fed, and legal challenges that could weaken or overturn the Humphrey’s Executor precedent protecting agency officials from removal without cause.

While the implications of these changes remain uncertain, they could have meaningful consequences for the Fed’s ability to operate independently. That’s the backdrop I want to expand on in this post. In particular, I want to highlight two major challenges currently facing the Fed—one rooted in political pressure, the other in economic uncertainty—that could also undermine its independence. I then will propose a simple solution that could offer the Fed a “safe harbor” in the midst of this current storm.

The First Challenge: Rising Political Pressure

The most immediate threat to the Fed’s independence is political, and it’s coming directly from the White House. President Trump has become increasingly vocal in his criticisms of the Fed. He wants Fed Chair Jerome Powell and the rest of the FOMC to cut rates to offset what appears to be a weakening U.S. economy: layoffs are starting, manufacturing orders are falling, producer prices are rising, confidence is stalling, economic growth forecasts are weakening, and stock prices are down. Ironically, all these developments can be traced back to the President Trump’s trade war. The worry is that more economic pain is coming. The obvious solution would be to end the trade war, but the President thinks the answer is with the Fed: cut interest rates already! And for good measure, incentivize these rate cuts by threatening to fire Fed chair Jerome Powell:

In case there is any uncertainty as to what he meant by these social media posts, here is President Trump in the White House on the same day:

He followed up with with more social media posts criticizing Chair Powell, but suddenly took a softer tone on April 22 when he said he never intended to fire the Fed Chair. This roller coaster ride of Fed criticism is probably far from over—as we first saw in 2018-2019—and likely to get more politicized as Powell’s term as Fed chair ends in 2026. The challenge this creates is how to protect the Fed from calls by the President to cut interest rates when they are not warranted.

The Second Challenge: How to Handle The Fed’s Dual Mandate When it is in Tension

The second challenge for the Fed is a familiar macroeconomic problem: what should the FOMC do when inflation is rising while the economy is slowing? This is the kind of policy dilemma that emerges from a negative supply shock, such as the pandemic or the new tariffs. These shocks raise production costs while simultaneously suppressing output, leaving Fed officials with few appealing policy choices. They also intensify the political pressures discussed above, as rising prices and weaker growth fuel public dissatisfaction and increase the temptation for politicians to scapegoat the Fed or push for more accommodative policies.

In theory, central banks should “look through” inflation caused by negative supply shocks, especially when it’s expected to be temporary. But things get trickier when inflation expectations aren’t well anchored and the shock has some staying power—say, because tariffs are snarling global supply chains and untangling them takes time. It puts the Fed in a tough spot: lean against inflation and risk deepening the slowdown, or stay on hold and risk losing inflation-fighting credibility. Either path could erode the Fed’s independence in this politically-charged environment. Chair Powell commented on this “challenging scenario” in a recent speech:

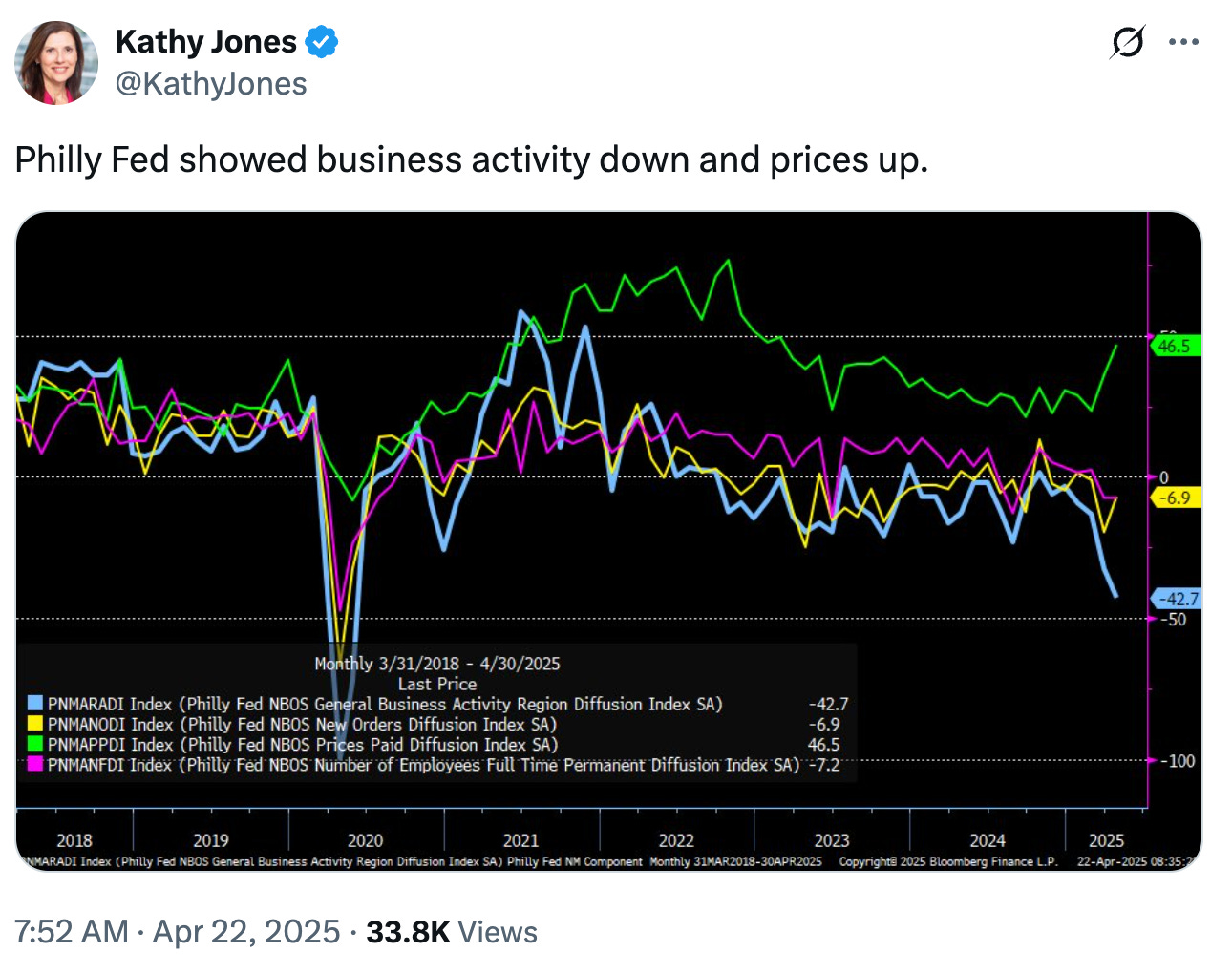

This “challenging scenario” isn’t theoretical—it’s already happening as Kathy Jones recently noted and is likely to get worse:

This is not a new problem for Chair Powell. The pandemic was a period marked by negative supply shocks disrupting production, global supply chains, and labor markets. Initially, it seemed relatively straightforward for the Fed to look through the “transitory” inflation created by these shocks. But the situation grew more complicated as those supply disruptions collided with historically strong demand pressures, fueled by expansive fiscal and monetary policy. The result was an inflation surge that proved far more persistent than the Fed had anticipated.

Chair Powell, in a November 2023 speech, had this to say about the lessons learned from this experience:

[F]or many years, it has been generally thought that monetary policy should limit its response to, or "look through," supply shocks to the extent that they are temporary and idiosyncratic… Our experience since 2020 highlights some limits of that thinking. To begin with, it can be challenging to disentangle supply shocks from demand shocks in real time… [Also, supply] shocks that drive inflation high enough for long enough can affect the longer-term inflation expectations of households and businesses. Monetary policy must forthrightly address any risks of a potential de-anchoring of inflation expectations

It is ironic that Chair Powell is once again facing the negative supply shock problem so soon after the pandemic. While he does not have to contend with historically large demand shocks this time, he does have to navigate rising political pressure from President Trump. If this challenge is not handled with care, it could further erode the Fed’s independence.

A Safe Harbor Solution

So we have two immediate challenges to the Fed that could undermine its independence: rising political pressure and tension in the dual mandate. Remarkably, there is a fairly simple solution that can meaningfully address both of these problems and create a safe harbor for the Fed.

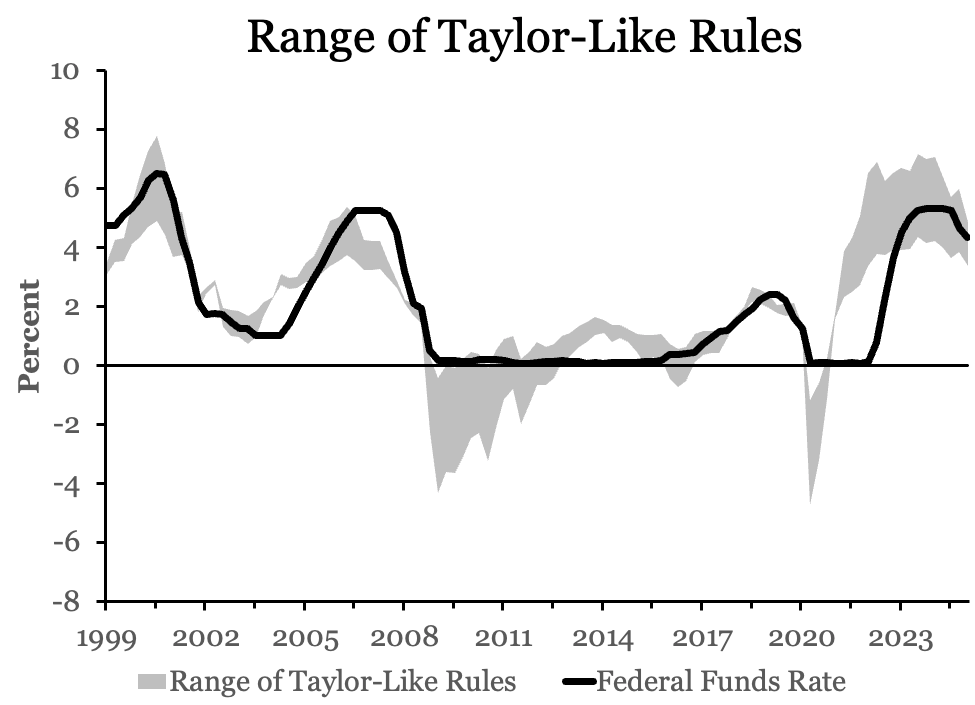

The solution is for the Fed to adopt and publicly commit to a benchmark range of monetary policy rules. These would not be binding mechanical formulas, but rather a transparent framework of guideposts that could inform and justify the Fed’s decisions. Crucially, it would not be just a single rule, but a range of rules calibrated to different assumptions and models. This diversity of rules would help preserve robustness and flexibility while still offering a disciplined policy anchor.

Such a framework would serve as both a shield and a compass. It would shield the Fed from political pressure by giving it a principled basis to push back against calls for rate cuts (or hikes) that aren’t justified by the data. Chair Powell could respond to political demands by pointing to the benchmark range and saying, “I hear you, Mr. President, but we’ve adopted this range of policy rules and are committed to following them. To deviate now would undermine our credibility.” At the same time, the rules would act as a compass by keeping the Fed oriented toward long-run policy goals, even during periods of heightened uncertainty or conflicting signals from its dual mandate.

To make this idea concrete, the figure below shows what such a benchmark range might look like. It presents a set of Taylor-like rules that incorporate different assumptions about the economy. Together, they form a plausible monetary policy rule range that could guide policy decisions and provide political cover in contentious moments. As of 2025Q1, the federal funds rate falls within this range—something Chair Powell could point to when criticized for not doing “enough.”

But not just any monetary policy rule will do. The benchmark range needs to be made of rules that are capable of handling negative supply shocks in a way that avoids overreacting to inflation while still preserving a credible nominal anchor. There is a framework that does exactly that: nominal GDP (NGDP) targeting.

NGDP targeting offers two key advantages over flexible inflation targeting. First, it makes it easier for the Fed to “look through” supply-driven price spikes, since this approach focuses the Fed’s attention on total dollar spending in the economy. This makes it particularly well-suited for navigating periods where inflation is rising and output is falling—the very dilemma the Fed is now beginning to face. Second, it anchors expectations around a stable nominal income growth path, giving households and firms a clear sense of the future economic environment without requiring the Fed to commit to unstable inflation-versus-employment tradeoffs in real time. Put differently, this approach allows the Fed to ignore short-term movements in inflation while still anchoring medium-run inflation. NGDP targeting, in short, would makes the Fed’s job a whole easier in this current environment. More details on NGDP targeting can be found here and here.

This very framework is what’s behind the rules shown in the figure above: a range of Taylor-like rules based on forecasts of the NGDP gap—a measure we report at the Mercatus Center that captures deviations of NGDP from its expected path. These rules vary by assumptions about the public’s forecast horizon but all share a common anchor in nominal income stabilization.

This kind of rules-based framework would provide guardrails during uncertain times and offer a steady anchor when political winds blow strong. In doing so, it could help preserve the Fed’s independence.

Conclusion

The Fed faces rising political pressure and growing economic uncertainty. In moments like these, discretion alone is not enough. By adopting a benchmark range of NGDP-based policy rules, the Fed could anchor its decisions in a transparent, credible framework—one that deflects political interference while still allowing room for informed judgment.

A rules-based safe harbor wouldn’t overly constrain the Fed. It would protect it by preserving both its independence and its effectiveness when they matter most.

CRITIQUE: I am a microeconomist, so i am wrong about little things, but isn't the easiest way to increase nominal GDP growth is to pump up the money supply? Didn't the Carter Admin do that which resulted in double digit inflation? And didn't Volker have to come in and raise interest rates to bring inflation expectations down. SUGGESTION: run this solution against post war data using standard macro models see how it would have performed.