More Buffer, Less Stigma: The Case for Discount Window Reform

Why integrating the Discount Window into liquidity regulation could reduce reserve demand, shrink the Fed’s footprint, and strengthen financial stability.

Can overprotecting the financial system make it more fragile? There appears to be a growing consensus that the answer is yes when it comes to the post-2008 liquidity regulations. These rules were intended to make the banking system safer by ensuring that banks had enough liquidity to withstand funding stress without first turning to the Federal Reserve. In practice, however, these regulations have encouraged banks to excessively self-insure and treat their liquidity buffers as untouchable hard minimums. The result is a banking system characterized by liquidity hoarding, a hollowed-out interbank market, and a large structural demand for reserves. This outcome can exacerbate periods of liquidity stress.

Moreover, these same regulations have also reinforced the longstanding stigma surrounding the Federal Reserve’s Discount Window (DW). Because banks are expected to meet liquidity needs with their own balance sheets, turning to the Fed for liquidity can be interpreted as a sign of weakness. This regulatory framework, therefore, further discourages the use of the DW while encouraging liquidity hoarding. Overprotecting the financial system can make it more fragile.

Several key policymakers have acknowledged these challenges in recent weeks. In this newsletter, I will highlight their concerns, discuss their proposal of integrating the DW into liquidity regulations, add a few more DW reforms to the mix, and respond to the moral-hazard objection raised against reforming the DW.

Policymakers Concerns and Solutions

The Board of Governors’ Vice Chair for Supervision, Michelle Bowman, gave a speech on March 3 that nicely motivates the issues at hand:

Fifteen years post-GFC, we need to know whether these [liquidity regulation] tools deliver the promised resilience or whether we have created a framework that looks impressive on paper but fails to capture the vulnerabilities that emerge in times of stress. It is time to move beyond asking whether banks are compliant and ask whether compliance actually translates into resilience.

Governor Bowman then notes that the liquidity regulations create two problems. The first problem occurs during normal times:

During normal times, banks over-allocate to HQLAs because they must demonstrate that liquidity needs can be met with their own balance sheet resources. At the same time, traditional Federal Reserve sources of liquidity—like daylight overdrafts, the discount window, and standing repo facilities—are stigmatized. This reduces a bank’s capacity to lend and support its communities.

The second problem appears during periods of stress:

During stress, the framework becomes pro-cyclical. Banks that maintain HQLAs at or above 100 percent of presumed outflows are often reluctant to use them out of concern they will fall below the minimum LCR. The LCR effectively becomes an isolated, unusable buffer. This reluctance exacerbates stress, forcing banks to convert less liquid assets into cash to meet obligations.

In short, the current liquidity framework may be making the banking system less resilient because it backfires in both good times and bad. It encourages banks to hoard liquid assets and avoid the Fed’s liquidity facilities in normal periods, while making liquidity buffers effectively unusable during stress because banks fear falling below regulatory minimums. In principle, the DW is supposed to serve as a liquidity buffer for the banking system, a backstop that banks can draw upon when funding pressures emerge. In practice, however, stigma has prevented it from playing that role.

Governor Bowman concludes by making the case that a modernization of the Federal Reserve’s DW so that it works with—rather than against—the current liquidity framework is a key step to solving these these challenges.

Treasury Secretary Scott Bessent and FDIC Chairman Travis Hill both pick up on this DW point in their recent speeches on liquidity regulation. Specifically, they argue that banks’ borrowing capacity at the DW should be recognized when assessing their liquidity positions.

Here is Secretary Bessent on March 3:

[T]he liquidity coverage ratio requirements [LCR] and other liquidity rules should give appropriate capped recognition of borrowing capacity associated with collateral prepositioned at the discount window.

And here is Chairman Hill on March 11:

[A]llow banks to recognize, up to a cap, their capacity to borrow from the Federal Reserve when calculating the LCR. This is a change the banking agencies could incorporate relatively quickly, yet thoughtfully, while still contemplating longer-term fixes to other aspects of the framework.

All three policymakers have more to say about Discount Window reform, but the central idea is clear: integrate the DW into the liquidity regulatory framework itself. Doing so would make the facility easier to use, reduce its stigma, and weaken the incentive for banks to hoard liquidity. Not only would this improve the DW’s functionality, but it would arguably lead to a more resilient banking system with less liquidity hoarding.

Do Banks Want Discount Window Reform?

Key policymakers seem eager to push Discount Window reform. But what about the banks themselves? Do they buy into the arguments outlined above? Fortunately, we do not have to speculate. Bill Nelson, Laurence Bristow, and Brett Waxman of the Bank Policy Institute recently surveyed their member banks to answer this very question.

The survey was conducted to determine what is driving the structural demand for reserves by banks and what could be done to reduce it. On the first point the authors note the following findings:

Survey respondents indicated that the main factors driving their demand were 1) internal risk management practices; 2) passing internal liquidity stress tests; 3) aversion to discount window borrowing and 4) the interest on reserve balances relative to rates on similar assets

These responses are revealing. They suggest that banks’ demand for reserves is not driven solely by market conditions but also by regulatory expectations and the continued stigma surrounding DW borrowing.

The survey then asked what changes would most effectively reduce banks’ demand for reserves. The authors summarize the responses as follows:

Treasurers stated that the three main changes that would be most effective at reducing their demand are: 1) allowing banks to anticipate borrowing from the discount window or Federal Home Loan Banks in their ILSTs; 2) counting discount window capacity toward the liquidity coverage ratio (LCR); 3) reducing discount window stigma.

Taken together, these responses align closely with the reforms discussed by policymakers above. Banks themselves appear to believe that better integrating the DW into the liquidity regulatory framework would lower the need for large reserve buffers (i.e. reduce liquidity hoarding). In short, this looks like a win-win for both policymakers and banks.

Beyond integrating the DW into liquidity regulations, there are other reforms that banks would likely support that could also reduce stigma and liquidity hoarding. First, the Fed could introduce a Committed Liquidity Facility (CLF), a pre-approved, collateralized credit line that banks pay a fee for and can draw upon as needed. This would give banks a dependable form of liquidity insurance that could also be recognized in liquidity regulations. Second, the Fed could revive a version of its Term Auction Facility (TAF), which would provide regular auctions of term credit to the banking system. Both reforms would help normalize use of the Fed’s DW. See Bill Nelson’s recent note for more details on these additional reforms.

Moral Hazard Concerns

Efforts to reduce Discount Window stigma and make it more accessible naturally raise concerns about moral hazard. As someone who generally prefers to see, on the margin, markets doing more and government less, I am often asked about this potential downside to DW reform. It is a fair concern.

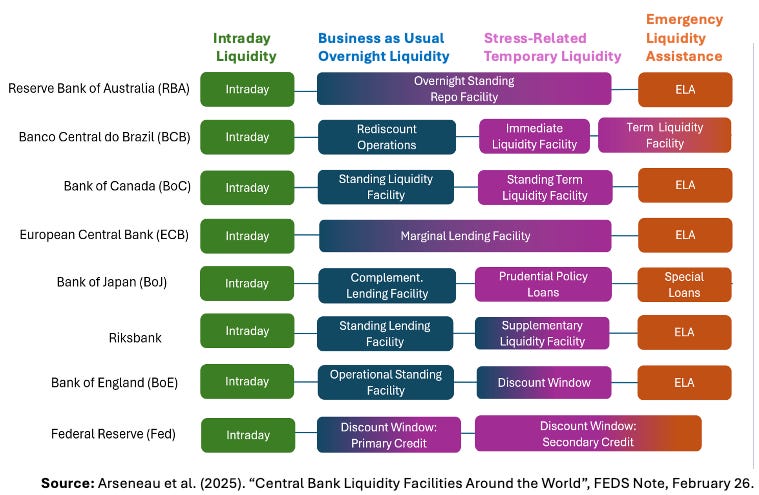

Here are my two responses to this concern. First, as this FEDS Note shows, most advanced-economy central banks already operate what are effectively “business-as-usual” liquidity facilities that banks can access on demand against collateral. These facilities are routinely used to help banks manage day-to-day liquidity needs and to support monetary policy implementation. As the figure below illustrates, central banks such as the Bank of Canada, the ECB, the Bank of England, and the Riksbank all maintain standing liquidity facilities designed for routine use. In this international comparison, the Federal Reserve stands out as something of an anomaly. Its DW is rarely used in normal times because of stigma.

Importantly, there is little evidence from this cross-country comparison that the routine use of these business as usual facilities has produced debilitating moral hazard problems. Instead, central banks manage the tradeoff between stigma and moral hazard through facility design: adjusting pricing, collateral requirements, and disclosure practices.

Second, the tradeoff between stigma and moral hazard must be weighed against other risks created by the current liquidity regulatory framework. As the policymakers discussed above emphasize, the motivation for Discount Window reform is precisely that the existing system may be making the banking system more fragile through liquidity hoarding and entrenched DW stigma.

Moreover, the current framework creates a larger structural demand for reserves and, as a result, a larger footprint for the Federal Reserve in the financial system. This expanded footprint is reflected in the absence of a robust overnight interbank market and an unusually large Fed presence in repo and Treasury markets. The resulting large Fed balance sheet also invites political scrutiny and can undermine the Fed’s independence.

For all these reasons, an analysis of DW reform that focuses only on the stigma–moral hazard tradeoff is incomplete and potentially misleading.

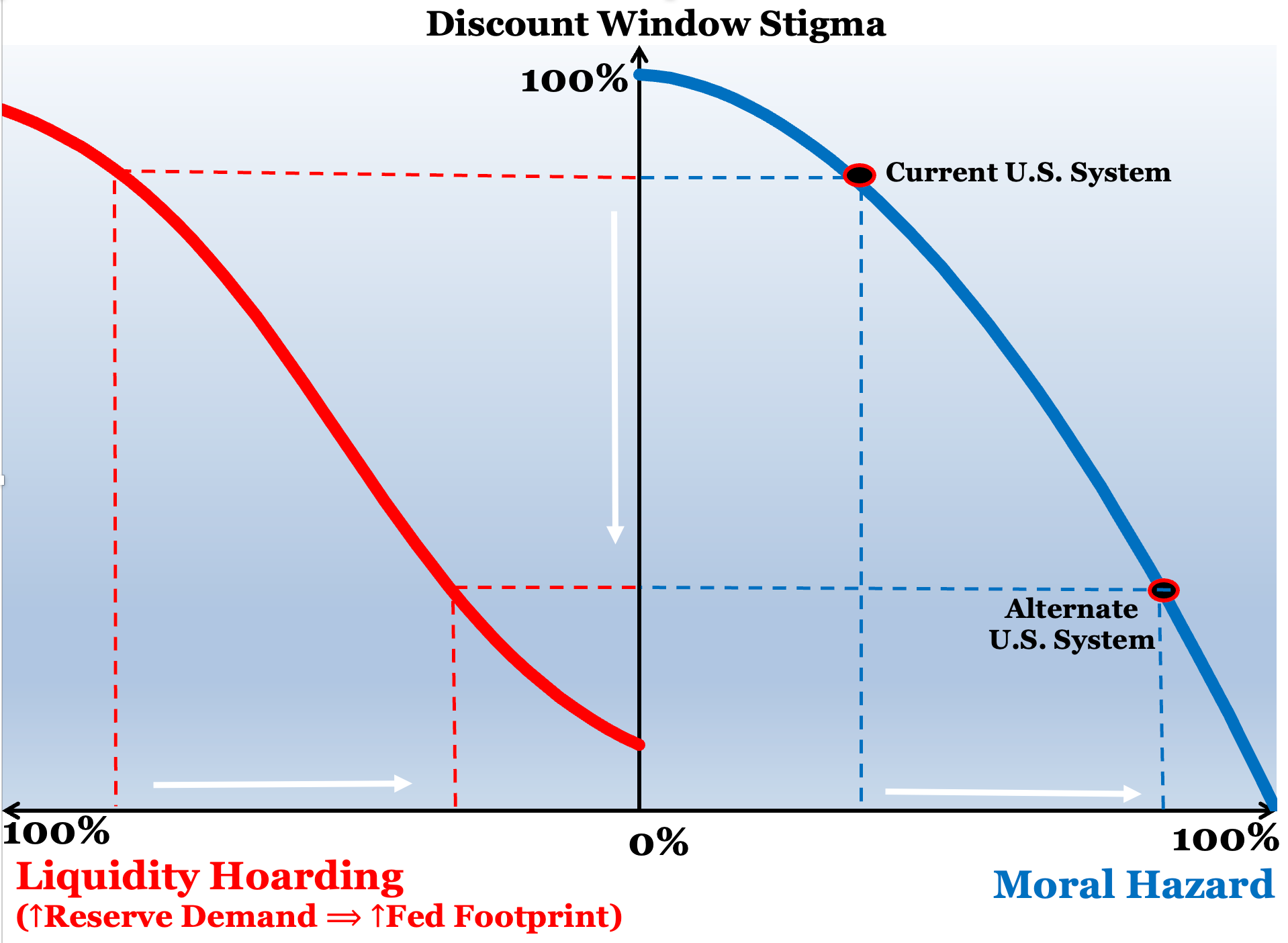

The multiple tradeoffs discussed above are illustrated in the figure below. Observers who focus narrowly on the stigma–moral hazard tradeoff are effectively looking only at the right-hand side of the diagram, represented by the blue curve. Their concern is that making the DW easier to use could increase moral hazard by encouraging banks to take on more risk.

While that concern is legitimate, it overlooks the left-hand side of the figure. Stigma does not simply reduce moral hazard—it also encourages banks to self-insure by hoarding liquidity, represented by movement along the red curve. That behavior shows up in the form of large reserve balances, weakened interbank markets, and a larger Federal Reserve footprint in financial markets. In other words, reducing stigma may increase moral hazard, but it can also reduce liquidity hoarding and its associated distortions.

As depicted in the figure, the current U.S. system sits in a region where stigma is high and liquidity hoarding is substantial. A reformed system would move the operating point downward along the curves by reducing stigma and liquidity hoarding even if moral hazard rises modestly.

Conclusion

Policymakers are increasingly recognizing that the post-2008 liquidity framework may have overshot its original goal. By pushing banks to self-insure against liquidity stress while stigmatizing central bank borrowing, the current system encourages behavior that can make the financial system more fragile. Integrating the Discount Window into liquidity regulations and normalizing its use would not remove every risk, but it could restore the facility’s intended role as a liquidity buffer for the banking system. The challenge now is to design reforms that manage moral hazard while reducing stigma. If that balance can be struck, the result may be a more stable financial system with more buffer and less stigma.

Great piece. As someone who's been writing about the need for these reforms for a few years now, great to see the recent resurgence of interest in these ideas!

Question: is it really worth it to reform the dw to work with a much broader liquidity framework that is as problematic as you say? Shouldn’t the framework be re-assessed as a whole?