Welcome to Macroeconomic Policy Nexus!

Our Journey Begins with Athanasios Orphanides

The Journey Begins

If you’re reading this, chances are you’ve listened to Macro Musings, followed my past blogging at Macro Musings (before it became the podcast’s name), or share my deep interest in macroeconomics, finance, and policy. Either way, I’m excited to have you here as I launch this new newsletter—a space where I’ll blend insights from my podcast and beyond with my original love for blogging.

This newsletter will land in your inbox twice a week. On Mondays, I’ll take you behind the scenes of that week’s Macro Musings episode—sharing key takeaways, extra insights from the recording, and sometimes even video clips that don’t make the final cut. On Thursdays, I’ll publish a second post highlighting recent economic developments, intriguing research papers, or policy debates that have caught my attention—an extension of the kind of macro commentary I used to blog about years ago.

This newsletter will be an exciting next step for longtime listeners of the show and those who have requested more regular content from me. I first entered the national conversation through blogging, so in many ways, this is a return to my macroeconomic roots. I'm coming back to writing with a decade of podcasting experience that has broadened my thinking and expanded my network of friends and fellow travelers. I invite you to join me on this journey by subscribing if you haven't already.

Before jumping into our podcast for the week, I thought it would be great for listeners of the show to get a behind-the-scenes look at where the magic happens. In the video below, you'll see the studio where Macro Musings comes to life—a conversation space that has hosted Nobel laureates, central bankers, and leading economic thinkers from around the world. This small room has been home to discussions that have helped shape broader conversations on monetary policy, financial stability, and macroeconomic theory. As we expand from audio into this written format, I wanted to share a glimpse of where it all began and where it continues to evolve. I hope this gives you a deeper connection to the conversations you've been following, and perhaps a new appreciation for the informal setting where we unpack some of the most important macroeconomic ideas.

For more videos like this, check out my BTS Instagram page!

This Week’s Podcast: Athanasios Orphanides

For this inaugural edition of Macroeconomic Policy Nexus, I’m excited to kick things off by highlighting this week’s Macro Musings guest: Athanasios Orphanides. A seasoned central banker and professor at MIT, Orphanides has spent decades studying monetary policy, both as a researcher and as a policymaker. His career includes 17 years at the Federal Reserve, where he worked on real-time policy analysis, and a term as Governor of the Central Bank of Cyprus (2007–2012), during which he was a voting member of the ECB Governing Council.

In our conversation, we dive into real-time monetary policy rules—a theme that runs through much of his research. Real-time rules use only the information available to policymakers at the moment decisions are made. Orphanides contends that central banks rely too heavily on unobservable and mismeasured economic variables, such as the output gap and the natural real interest rate, when making decisions in real time. He makes the case that policymakers should instead focus on rules that are robust to uncertainty, such as his preferred “natural growth targeting” framework, which adjusts interest rates based on deviations of forecasted nominal income growth from its ‘natural growth’.

We also revisit the lessons of the 1960s and 1970s inflation episodes, discussing how misjudging economic slack contributed to policy errors that led to runaway inflation. In fact, Orphanides has famously shown (ungated version) that had the Fed followed the Taylor rule in the 1970s using real-time data, they would not have acted much differently than they actually did! They would have implemented the same overly accommodative monetary policy that raised the trend inflation rate. So, be wary of using real-time estimates of the output gap and the natural real interest rate in setting monetary policy!

Orphanides also draws parallels to recent Fed policy, particularly how the asymmetric approach to employment introduced with FAIT—the Flexible Average Inflation Target—and the use of forward guidance to implement it may have amplified inflationary pressures. He also shares insights on what a better monetary policy framework might look like—including greater transparency around simple rules to constrain discretion and avoid major mistakes.

A Closer Look at Monetary Policy Uncertainty

As noted above, a key point that Orphanides makes is that real-time measures of the natural real interest rate and output gap are subject to big revisions. Consequently, it is best to minimize their use when implementing monetary policy. To illustrate this problem, consider the 1993 Taylor Rule. As seen below, it requires real-time estimates of the natural real interest rate—embedded in the neutral nominal rate via the Fisher equation—and the output gap:

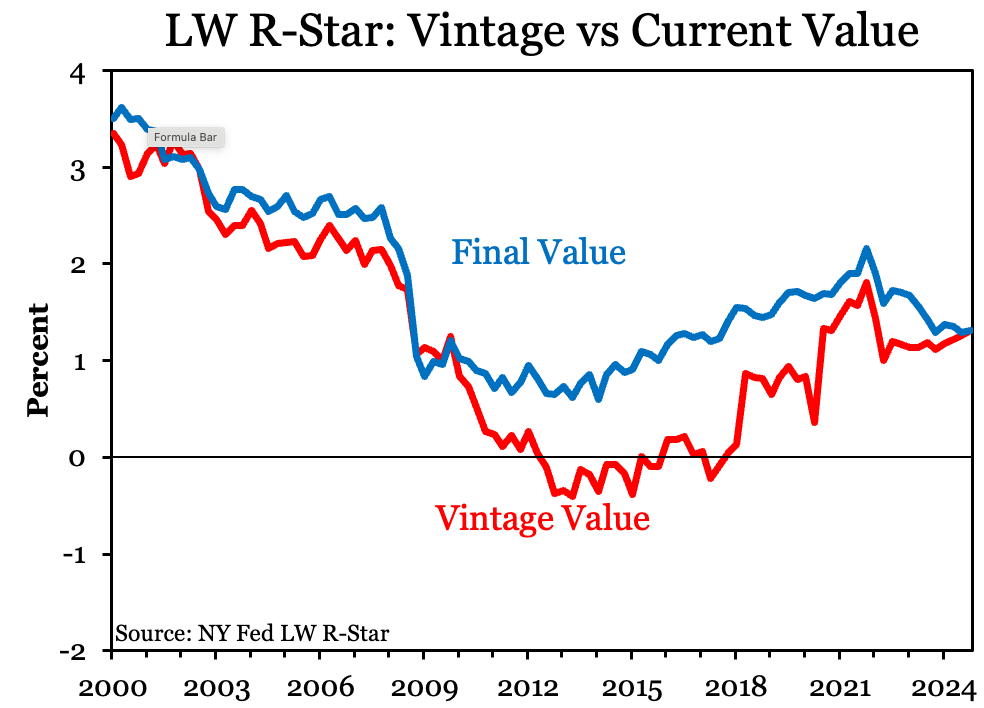

Since the Taylor Rule needs both unobservable series as inputs, this reliance creates uncertainty around its prescribed target interest rate. The uncertainty is driven by the revisions between the vintage (real-time) values of these variables and their current values. This can be seen in the figures below. The first one shows the famous Laubach-Williams R-star estimates from the New York Fed. The change in value from revisions are particularly large for this series in the 2010s, averaging about 0.9 percentage points in absolute value. Overall, the change from revisions average 0.6 percentage points (Note that revisions get smaller at the end of the sample. This is because real-time values are the current values)

The next chart shows the revisions to the output gap estimates from the Tealbook (formerly Greenbook) produced by the Fed staff for the FOMC meetings. This information is only available up through the end of 2019, so I use the CBO output gap estimates from 2020-2024. Here too we see meaningful revisions that average 0.9 percentage points in absolute value.

Orphanides recommends two workarounds to these measurement problems. First, use difference equations in your analysis. That is, look at monetary policy rules that use changes in the target interest rate rather than its level as the instrument. Doing so eliminates the intercept term—the nominal neutral rate—since the monetary authority is now responding to changes, not levels, in this setup. Second, target a growth rate rather than a level variable since the former has smaller revisions. Orphanides specifically recommends an approach he calls ‘natural growth targeting’:

In this equation, there is only one unknown variable and it is in growth rate terms: the natural growth target. Orphanides sets this equal to the expected growth rate of potential real GDP over the next year—period t through t+3—plus 2% for the inflation target. In other words, Orphanides is looking at a neutral nominal income or ngdp growth rate expected over the next year. There are various ways to get estimates of potential real GDP over the next year. Below, I construct a measure of it using CBO forecasts. Here too, there are revisions but the magnitudes are notably smaller. They average only 0.3 percentage points in absolute value.

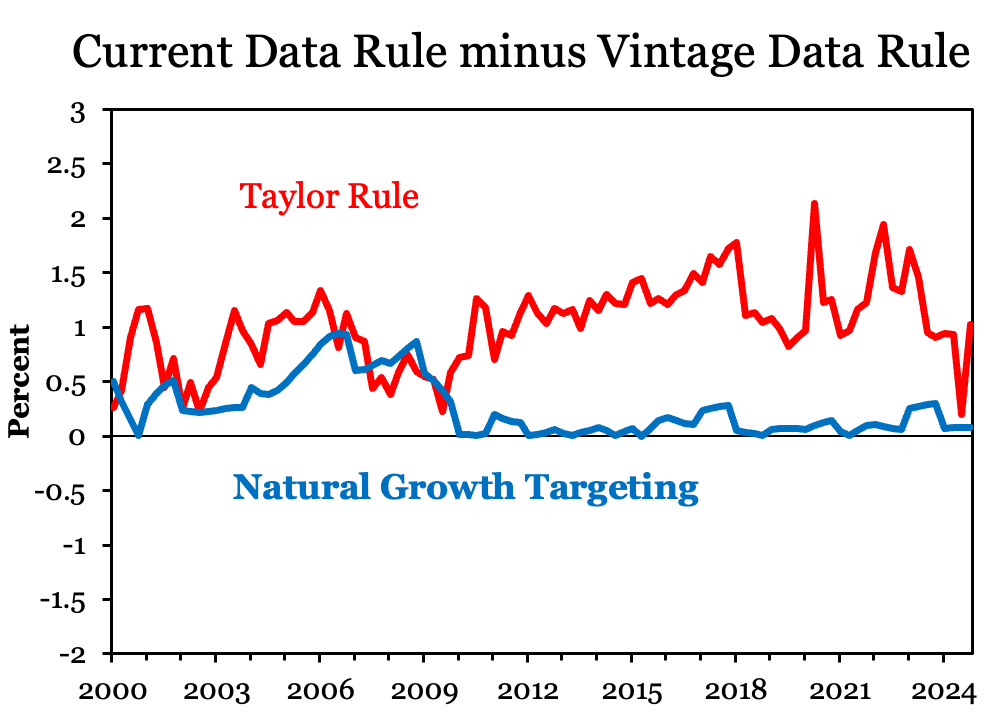

Now, let’s take these two rules and plug in the vintage values and the current values. Then, we can examine how much the prescribed policy rule values would change between the two series. The figure below illustrates this by showing the difference the vintage data rule from the current data rule:

As the figure makes clear, revisions to the Taylor Rule are relatively large, averaging 1.02 percentage points. The revisions to the natural growth targeting rule, by contrast, average 0.13 percentage points. Now as listeners of the podcast know, I am fan of nominal income targeting so this makes me happy!

However, I am more of a fan of NGDP level targeting since I think makeup policy is extremely important in ZLB environments as well as for supporting financial stability. So, how would a NGDP level fare against Orphanides’s natural growth targeting rule in terms of revisions? I tried two different versions of a nominal income level target. First, I constructed a level version of Orphanides’s rule. Let’s call it ‘natural level targeting’. For my natural level target I used the forecast of the neutral level of NGDP that comes from the Mercatus Center’s NGDP Gap series.

Second, I also used a more standard NGDP level target rule where the policy rate is in levels and the there is an intercept term:

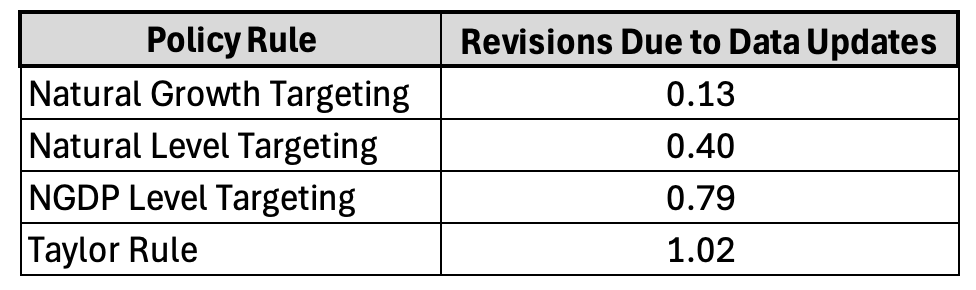

Okay, so below are the revisions to the various rules due to changes from the vintage data to the current data for the 2000-2024 period. The results, like before, are in percentage point changes in the policy rate. Oprhanides wins this horse race by a long shot! His nominal income growth rule beats out my two nominal income level rules. I have to confess this gives me pause. On one hand, I still am convinced level targeting is important for macroeconomic stability. On the other hand, implementing level targets in realtime may cause policymakers to make mistakes given the data revisions. This is a tough one to navigate.

David, I don´t think the problem with level NGDP targeting has much to do with data revisions. Take 2008. The Fed "purposely" tanked down the stable level path that had "endured" for more than 15 yrs. To try to go back would have shown everyone that the Fed had messed-up, an historical no-no!. Instead, Bernanke was lauded as "saviour" for avoiding a second Great Depression, but few saw that he had "engineered" a Long one. After Covid-19 hit, Powell got NGDP back very quickly to the previous trend. The drop, as everyone knew was the fault of Covid. He brought the NGDP level above the previous one, getting a little closer to the original one. Powell should try to keep NGDP riding along this new trend. My latest, with links to this question:

https://marcusnunes.substack.com/p/macroeconomic-cycles-over-the-past-a17

This will be a godsend as I despise "listening to" economics. I need to constantly stop and say, "What??? That can't be true" and the work out how it could be true.

The lesson I take from your write-up of this session is whether the policy maker should be optimizing and running a risk large errors or satisficing to do well enough with less chance of error